Generally speaking, investors face two choices: being a part-owner of businesses around the world (stocks) or lending money to companies and governments (bonds). Funds are simply combinations of stocks and/or bonds in a mix that meets the mandate of the respective fund.

There is a set number of listed stocks and available bonds, yet – interestingly – there are more stock funds than there are stocks themselves! The investment industry is increasingly competitive, and the number of funds available continues to rise – it is evident that having a sensible process for selecting what funds should be included in an investor’s portfolio is key to investing success.

Cutting through the complexity and noise is a task that our firm’s Investment Committee does not take lightly – a comprehensive whole-of-market fund screening process takes place on a regular basis. This process ensures that we remain confident that the funds recommended to you are ‘best-in-class’, offering the best chance of a successful investing experience.

Some investors assume that more funds must be better. Managing the risk exposure of a portfolio with 20 or more funds can be challenging for any investor. It can feel reassuring, as if adding extra funds automatically deepens diversification. The reality, however, is that the underlying stocks and bonds within the funds held are what provide the returns (and risk) to investors – therefore holding multiple funds may simply adjust the weights of what is already held or even double up on exactly the same stock and bond exposures[1].

This may be intentional and additive, but it can also create unnecessary complexity and duplication. Take, for example, two funds capturing the returns of the US stock markets. Some may naively hold both, assuming that diversification is improved, though if one offers better alignment with one’s goals (e.g. lower cost, longer track record, meets performance parameters closer) then it raises the question of why this is not selected alone.

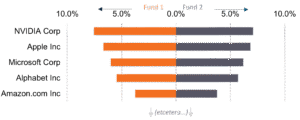

Figure 1: Largest five holdings of two US stock market index tracking funds

Source: Fidelity Index US Fund (left), Legal & General US Index Trust (right). For example purposes only. Not a recommendation.

Clearly, splitting an allocation between both funds adds little to no value to investing outcomes, as the holdings are virtually the same.

In certain situations, holding multiple funds may contribute positively to an investment strategy. For instance, investors seeking to enhance expected returns by targeting small-cap or value companies can utilize a selection of funds that adjust allocations to underlying stocks, thereby offering a ‘tilted’ exposure to these specific attributes.

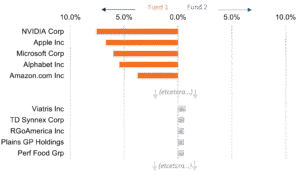

Figure 2: Largest five holdings of US stock market index tracking fund, and small cap value fund

Source: Fidelity Index US Fund (left), SPDR MSCI USA Small Cap Val (right). For example purposes only. Not a recommendation.

Investors seeking a sensibly structured portfolio for the long term are not required to own an unnecessary number of funds to do so. Simplicity does not mean a lack of sophistication. Choosing the best funds for their designated role – and monitoring them regularly through time – is key to investing success. This responsibility sits within the remit of our Investment Committee and forms part of the regular review process of the investment solution we recommend to you.

Beware of unnecessary complexity, disguised as diversification.

Everything should be made as simple as possible, but not simpler

Albert Einstein

Important notes

This is a purely educational document to discuss some general investment related issues. It does not in any way constitute investment advice or arranging investments. It is for information purposes only; any information contained within them is the opinion of the authors, which can change without notice. Past financial performance is no guarantee of future results.

Products referred to in this document

Where specific products are referred to in this document, it is solely to provide educational insight into the topic being discussed. Any analysis undertaken does not represent due diligence on or recommendation of any product under any circumstances and should not be construed as such.

[1] Note that investor assets sit in a ringfenced custodial account – not on a fund manager’s balance sheet. Splitting allocations between managers on this basis should not be a concern, ceteris paribus.