taken from an article by EBI Portfolios…..

Harold Macmillan, the UK Prime Minister between 1957 and 1963 was reputed to have replied “events dear boy” when asked what the most likely thing would be to knock his government off course. With the increased focus on Sustainable and Socially Responsible investing it now seems that there is significant “event risk” involved in running a company in contravention of these principles and the bigger and more high profile it is, the more dangerous things can get.

The world seems more than ever eager to take offense. What would once be dismissed as a joke or mild criticism is now portrayed as something akin to assault, regardless of the intent behind the statement. The resignation of Alastair Stewart in recent days as a result of a (somewhat concocted) row on Twitter with another user is but one in a long list of the famous who have been brought low by controversy.

It has, in recent years become a business issue too. Once upon a time, executives had to be wildly ill-judged in their comments to make the headlines, but it appears that they too are now having to be extremely careful in their public utterances, lest it create a firestorm of negative publicity.

This is less true in the financial industry, which seems still stuck in the 1950’s in terms of its outlook; but things may at last be changing, at least a little; in November last year, it was reported that Ken Fisher (the billionaire chairman of Fisher Investments) made a series of offensive remarks at a Conference- he probably thought they would not be repeated outside of the room, but they were- and when they were, the LA Fire and Police pension fund, Iowa State pension fund, Goldman Sachs and Fidelity Investments pulled nearly $3 billion in total from his firm in a matter of days. What might have once been ignored was now a potentially business-threatening error.

Shareholders, under pressure from their investors, appear to be baring their teeth too. In the same month, (November), Brooks Macdonald saw its director’s pay structure hit by a shareholder rebellion, with nearly 40% of shareholders voting against it, while 42% of shareholders voted against the planned pay award for its in-coming CFO, Stephanie Bruce. Elsewhere, Fidelity found itself at the centre of controversy, after it was found, (by the Sunday Times), that they were promoting funds as “ethical” when they were in fact no such thing- only 1 of the 49 funds described as “socially responsible” actually met the criteria for being so described. Drinks firms, defence companies and even tobacco manufacturers all featured in these funds, some of whom were their biggest holdings. In a statement to the newspaper, the Fidelity Head of personal investing blamed third party data providers. ‘We take the accuracy of our platform data extremely seriously and we are concerned that there may be an error with this particular data feed provided to us’ they intoned gravely. In what was a busy November for activists too; lawyers acting for clients of Woodford Income fund investors announced that they were suing Hargreaves Lansdown for, amongst other things, mis-representing the health of the fund as a result of the close business relationship between the two firms. In the same month, it was revealed that the Chief Executive of McDonalds had been fired over a (consensual) relationship with another employee, which violated company policy. More recently, the same thing happened at Blackrock, the fund management giant. (With Larry Fink, the firm’s Chairman openly espousing “Sustainability” as part of their investment process, they could not really do anything else).

But all this represents a sea-change in attitudes, something which it appears executives are struggling to get to grips with. Some are adapting better than others.

Most obvious pitfalls are clearly avoidable, but top level bosses appear unable to stop themselves; the Boeing 737 Max crisis, erupted when two plane crashes in quick succession were met with denial and corporate doublespeak, with executives insisting that the plane was safe. Internal e-mails from both current and former employees painted a damning picture of a firm that was engaged in withholding information from the FAA (the US airlines regulator), whilst cutting development costs to meet shareholder targets. One senior engineer complained that “Boeing management was more concerned with cost and schedule than safety or quality.” The result has been to gift leadership of the industry to Airbus, as even Boeing test pilots have admitted that they would not want their family and friends flying in the plane [1].

Others though are not so easy to anticipate- Gillette, the maker of razor blades, probably thought they were on to a winner by backing the #MeToo movement, in a series of adverts decrying “toxic masculinity”. According to PR Daily.com the number of “dislikes” of its series of videos, at 265,000, was more than six times the number of “likes”. They may have inadvertently created an ”issue” where none previously existed, which might indicate the dangers of taking a political stance, rather than remaining neutral (or as close as is possible) on matters tangential to the business itself.

Similarly, it is hard to see how SRI/ESG investment policies would have saved Nissan (and its shareholders) from the controversy surrounding the arrest, sacking and subsequent flight to Lebanon of its formerly feted boss Carlos Ghosn. Car firms are making significant efforts to create “green” vehicles, such as hybrid and fully electric cars, thus avoiding (most) of the hurdles imposed by ESG related filtering criteria- but there are some events that cannot be adequately modelled or assessed and it is important to remember that ethical filters are not a panacea for all ills.

Here in blighty, the Guardian newspaper has become the first journal of record to ban fossil fuel advertising from its pages. Oil and Gas firms are at the forefront of the assault by ESG/SRI activists, as the UK does not have any cluster bomb manufacturers. This may be the start of a concerted PR campaign against the industry, one that it is not clear that they can entirely placate.

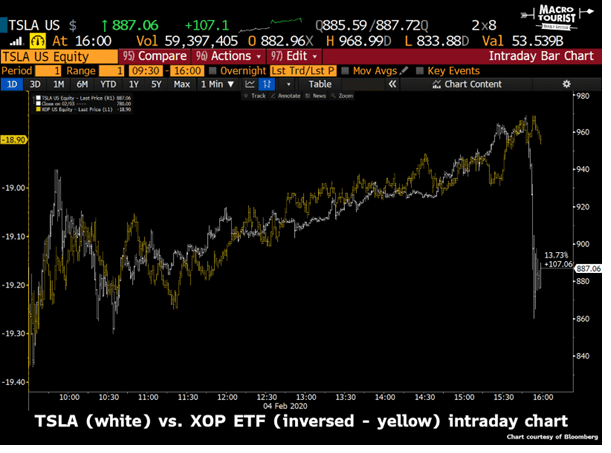

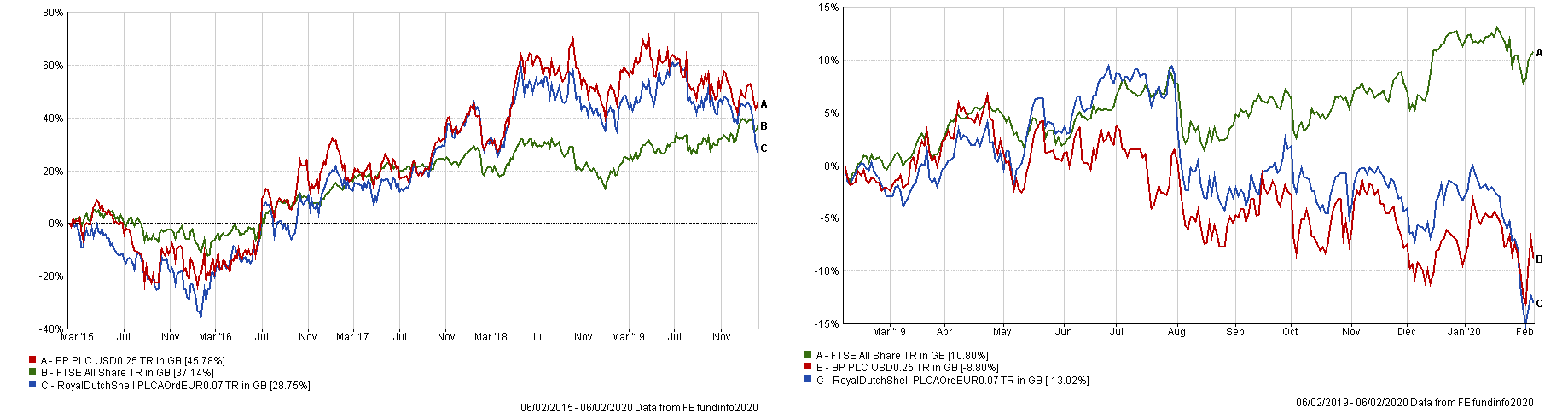

In theory, this could lead to a systemic decline in the share price of Oil majors such as BP, Shell etc. It appears that this is already underway, at least over the last year. How much of that is to do solely with the oil price is hard to say though. In the US, the energy sector now represents less than 4% of the S&P 500 Index and this weighting could easily fall further. Notably, the recent stellar rise in shares of Tesla, the only truly “green” auto manufacturer has gone hand in hand with the fall of Oil shares (see chart below)- are the big institutional players finally getting into Tesla (and out of Big Oil)? The chart shows only one day’s worth of data, but it might help explain the near vertical rise of Tesla in the last 2-3 weeks, as Institutions find it hard to source stock from the market; and as they buy Tesla, they sell out of oil shares. After the near 20% fall in the Tesla share price on Wednesday however, one might question the timing of the decision, but when big investors decide to buy sometimes in large size, they need to be in, and price becomes a secondary issue for them.

[XOP is the code for the S&P Oil and Gas Production and Exploration ETF].

Of course, what could happen (eventually) is that the risk premium on oil shares becomes attractive enough to justify buying them- albeit potentially at much lower prices. At some price point, they become cheap enough to justify buying, though, given the institutional pressures fund firms are facing, it may be that private investors, rather than institutional fund managers reap the benefits, as the latter may feel constrained by their public ESG/SRI stances.

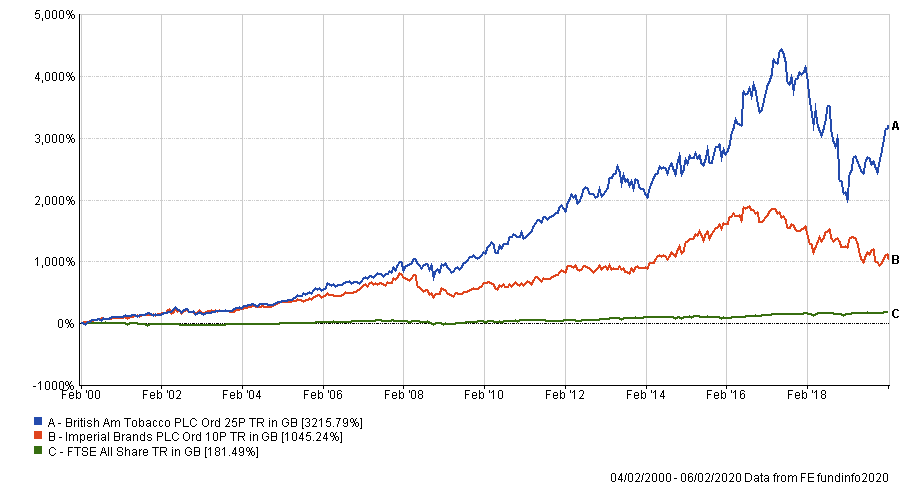

We have seen this phenomenon with Tobacco shares over the majority of the 21st century. Despite their terrible public persona, they have massively outperformed the All Share Index since the turn of the century. The same thing could happen to oil firms too- then again maybe they are truly doomed.

But for those inclined to adopt an ethical approach to investing this may be largely beside the point. The aim is to reduce (and ideally eliminate) event risk- idiosyncratic risk in the jargon and in this sense it is perfectly possible to understand why ESG/SRI would not necessarily lead to underperformance vis-à-vis conventional Indices- if you don’t own Shell and one of its tankers deposits a large amount of oil into the English channel, you would be almost sure to outperform both the FTSE 100 and likely the All Share Index too. These sorts of events do not happen often (thankfully, but the share price of BP has gone essentially nowhere since the Deepwater Horizon disaster of April 2010 [2]), and when it does, it can take a long time for a share price to recover; indeed, given the present zeitgeist, they may not recover at all…

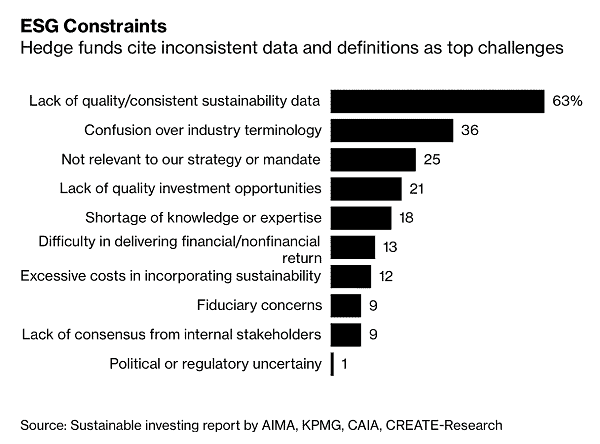

For now, though, more practical issues remain. According to this survey of Hedge funds, the lack of consistent, high quality sustainability data is the biggest impediment to widespread adoption of ESG/SRI policies amongst the investment community. If and when this is resolved, there is long way to go before sustainable investing peaks…..

[1] It hasn’t worked out too badly for the CEO, however- Dennis Muilenburg left with no severance pay, but a $62 million equity and pension benefits package to cushion the blow of being fired. Shareholders don’t seem too concerned either- the share price is above the $320 level (now c.$340) that it was in November 2018, when the first crash occurred.

[2] As of the end of April 2010, as the explosion occurred, the price was £4.94. As of 6/2/2020, the total return since then has been 28.67%. In the same period, the All Share Index has risen by 40% in price terms, for a total return (which includes dividends) of 99.5%.