When you invest in assets from other countries, the value of those assets can change because of how different currencies move against each other. For example, if you own US shares and the US dollar gets weaker compared to the British pound, your shares might be worth less in pounds, even if their value in dollars hasn’t changed.

It’s natural to wonder what to do about this “currency risk.” You have two main choices:

- Accept the risk: Just let currency movements affect your investments.

- Transfer the risk: Pay someone else (like an investment fund) to take on this risk for you. This is called ‘hedging’.

The best choice depends on what role the investment plays in your overall financial plan.

So far in 2025, many major currencies, like the Australian Dollar, Canadian Dollar, British Pound, Japanese Yen, and Euro, have become stronger against the US Dollar (up between 5-12%)[1]. This has made investors think more about how currency changes affect their global investments.

Most people who try to make money by guessing currency changes lose money. Websites for currency trading often warn that most traders don’t profit[2].

Because it’s so hard to guess which way currencies will go, you should only decide to accept or transfer currency risk if it will really affect how well an investment does its job. For example, if it stops your safe investments from actually being safe. Let’s look at this in more detail.

The Two Main Parts of Your Investment Portfolio

Your investments are generally split into two main types:

- Growth Assets: These are designed to grow your money over time (like stocks).

- Defensive Assets: These are meant to provide stability and protect your money when the economy is struggling (like high-quality bonds).

Defensive Assets

Why it’s important to protect your defensive assets from currency risk

For defensive assets, like high-quality bonds, currency risk can be much bigger than the risk of the bond itself. Because of this, it’s very important to protect these investments from currency changes.

We do this using something called ‘currency hedging’ within the investment funds. This means we try to remove the impact of currency movements from your returns. The chart below shows how much less risky overseas bonds become when their currency exposure is hedged.

Figure 1: Comparing bonds with and without currency protection

Data source: Payden Global Government Bond Index, iShares Global Government Bond ETF, Vanguard Global Stock Index. Period: 01/04/2011 – 31/05/2025. Returns shown in GBP.

Defensive assets are there to keep your portfolio steady. If they are exposed to currency changes, they might not be as stable. Even though hedging costs a bit extra, it makes these investments much less volatile. This ensures your defensive assets do their job, especially when markets are down.

Growth Assets

Deciding what to do with currency risk is less clear for growth assets

For growth assets, which are usually stocks, it’s not as clear whether to hedge currency risk. Unlike with defensive assets, hedging currency in growth assets doesn’t always make them less risky overall. It just changes how currency movements affect your returns.

Historically, how currency movements and global stock markets relate has been different in various markets, making outcomes hard to predict. The ups and downs of currency markets and stock markets are often similar over time.

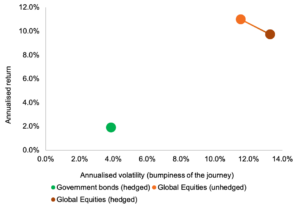

Figure 2: Comparing stocks with and without currency protection

Data source: Payden Global Government Bond Index, iShares MSCI World GBP Hedged ETF, Vanguard Global Stock Index. Period: 01/04/2011 – 31/05/2025. Returns shown in GBP.

By not hedging currency in growth assets, you avoid the extra cost of hedging. Another important point is that when there’s high inflation in your home country, your local currency usually loses value. This means that your overseas assets, when converted back into your local currency, are worth more of that weaker currency. In short, owning unhedged overseas stocks might (but it’s not guaranteed) offer some long-term protection against high local inflation. Also, it can be hard to find hedged investment products for all types of growth assets.

All things considered, it often makes good sense to leave the currency exposure in your growth assets unhedged.

Three Key Things to Remember About Currency Risk

- Protecting your defensive assets from currency changes is a good way to make them more stable.

- For growth assets, hedging currency isn’t expected to make you more money or reduce risk, and it might add complexity and costs.

- Don’t try to guess currency movements – very few people, if any, can do this reliably.

General Investment Risk Warnings

Please remember the value of your investments and any income from them can go down as well as up and you may get back less than the amount you originally invested. All investments carry an element of risk which may differ significantly.

If you are unsure as to the suitability of any particular investment or product, you should seek professional financial advice. Tax rules may change in the future and taxation will depend on your personal circumstances. Charges may be subject to change in the future.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated. Portfolio performance data are for illustrative, educational purposes only and do not represent live client portfolios.

[1] Source: Koyfin as at 12/06/2025. All rights reserved.

[2] See ig.com, trading212.com, and etoro.com as examples