Whilst on the face of it, the State Pension can seem fairly straightforward, successive governments have changed the way it’s calculated and when you build up entitlement. So, it can be a little more complex than you may expect.

Even if you’re saving into a private pension or making other provisions for retirement, the State Pension is important. It’s a reliable source of income throughout retirement that can act as a foundation to build on.

If you’re nearing retirement, it pays to understand what you can expect to receive and when; it could change your retirement plans. Even when retirement is some way off, getting to grips with your State Pension can help make sure you don’t have any gaps in National Insurance contributions that could affect your future income. It’s never too early to start thinking about your State Pension.

The history of the State Pension

The UK State Pensions goes back a little more than 100 years, but it’s a concept that’s been around far longer.

As a Roman Centurion completing active service around 100 AD you could expect to receive a regular income for the rest of your life, a payment known as an Annuity and a term we still use today when it comes to private pensions. It took many centuries for the origins of the modern-day pension to emerge.

The Old Age Pension was introduced in the UK back in 1908 for people aged 70 and over and was means-tested. With lower life expectancy, just 500,000 claimed this pension of five shillings a week. It might not be as valuable as the State Pension offered today, but it was a good foundation to build on.

In 1925, a new kind of pension was introduced, based on contributions paid at work by employers and employees. It wasn’t means-tested and could be claimed from the age of 65. A married couple’s rate of pension was paid when both husband and wife reached 65 or more. So, in 1940, the pension age for women fell to 60 to try and ensure that for most couples, the married rate would be paid when the husband reached 65. This difference between men’s and women’s State Pension age has only recently been addressed.

Linking the State Pension to National Insurance contributions, as it is now, occurred in 1948. Whilst some changes have continued to be made to the State Pension over the last seven decades, the foundations of the State Pension and the goal to provide a basic level of income to those in retirement has remained the same.

Understanding your State Pension

When thinking about your State Pension, there are two key questions to ask:

- When can I claim the State Pension?

- How much State Pension will I receive?

The State Pension age

The State Pension age is the point that you can start claiming your State Pension.

It was decided in 1995 the State Pension age for men and women should equalise. As a result, between 2010 and 2018 the women’s State Pension age gradually increased until it reached 65. It meant that some women born in the 1950s had to wait longer than expected to receive their State Pension.

Now that the State Pension age is the same for men and women, it might seem like it should be straightforward to provide a date when you can claim. However, as life expectancy increases and the cost of delivering the State Pension rises, the milestone has been moving upwards too.

By October 2020, the State Pension age for all will reach 66. There are also further planned increases for it to reach 67 by 2028 and 68 by 2046. These dates are currently under review and they could change in the future. As a result, it’s important to know when you’re expected to reach State Pension age now and ensure you keep up to date with government changes that could affect your plans in the future.

The government’s State Pension calculator will tell you when you’ll reach State Pension age under the existing plans. You can find it here.

How much will you receive through the State Pension?

In 2016 the new flat-rate of State Pension was ushered in. It was designed to make it simpler to understand, but for some approaching retirement, the reality is still far from simple.

How much State Pension you’ll receive will depend on how many qualifying years of National Insurance contributions you have. This will include the years you paid National Insurance whilst employed but it is also possible to build up credits when you’re raising a family, in full-time education or caring for someone that has a disability.

You can check your National Insurance record here. If there are gaps, it is often possible to make voluntary contributions to bridge this. However, be aware that this doesn’t always increase the amount of State Pension you receive, so be sure to check first.

To receive the full State Pension, you must have 35 qualifying years on your National Insurance record. For the 2020/21 tax year, those receiving the full State Pension will receive £175.20 per week, or £9,110.40 annually.

To receive any State Pension at all, you must have a minimum of 10 years of National Insurance credits. If you have between 10 and 35 years, you’ll receive the equivalent value of your State Pension according to the number of years built up. So, if you have 23 years on your record, you’d receive roughly two-thirds of the State Pension or about £117 per week.

Keeping pace with inflation

The good news is that the State Pension rises each year, thanks to the triple-lock system. This helps your State Pension income keep pace with inflation and preserve your spending power. The State Pension increases by the highest of three measures:

- Price inflation

- Average earnings growth

- 2.5%

As a result, your State Pension income will rise at the start of every tax year by at least 2.5%. For the 2020/21 tax year, the State Pension increased by 3.9% matching the average earning increase seen by UK workers in July last year.

Why your State Pension could be higher or lower than expected

In addition to National Insurance credits, two areas could affect how much you receive.

Additional State Pension

It’s no longer possible to build up additional State Pension. However, the government has allowed many workers to keep their existing entitlement built up between 1978 and 2016, thereby increasing the amount they’ll receive when they reach retirement age. It’s something that could affect workers that are still several decades away from retirement.

Additional State Pension is also known as the second State Pension, S2P and SERPS. This now redundant option allowed people to top-up their basic State Pension. Understanding what additional State Pension means for your retirement income can be difficult. It involves a ‘starting sum’ calculation that compares your entitlement under the old and new regime, you’ll then receive the higher of the two. If you have any questions about SERPS and your retirement, please get in touch.

Contracting out

Contracting out of the State Pension was abolished in 2016. However, if you’ve contracted out in the past, it could still affect how much you’ll receive. In some cases, workers have not known they were contracted out, so it’s important to check.

Contacting out means workers paid a lower rate of National Insurance contributions. In return, they would have paid this money into their workplace pension scheme, or their employer would have done so on their behalf. In most cases, those affected by contracting out have a Defined Benefit pension scheme (also known as a Final Salary Pension). You can check if you were ever contracted out here.

How does the State Pension fit into retirement plans?

The State Pension isn’t something that should be looked at and reviewed alone. Instead, it’s important to assess it alongside other retirement plans, private pensions and other provisions.

For example, it could boost the income you’ll receive from a Final Salary pension, allowing you to meet aspirations that you previously thought were out of reach. Alternatively, you may have decided to access a Defined Contribution pension through drawdown and the State Pension means you can reduce withdrawals and still maintain your lifestyle, helping your private pension go further and perhaps leave a legacy for loved ones.

Understanding your State Pension and the stable income it will deliver for the rest of your life can provide confidence as you plan retirement too. It’s a safety net that can ensure essential outgoings are met and help you achieve the retirement lifestyle you’ve been looking forward to.

Financial planning can help you build a retirement plan that brings together the different strands of income you’ll have access to, from the State Pension to an investment portfolio.

Your State Pension checklist

- Check when you’ll reach State Pension age here

- Review your National Insurance record here

- See if you were contracted out of the State Pension here and review if you have ever made additional State Pension contributions

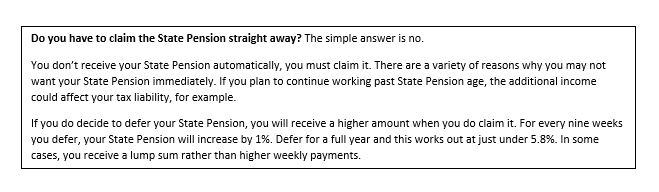

- Decide when you want to claim your State Pension, information on how to do so can be found here

- Incorporate your State Pension into your wider retirement plans and finances